Posted on 9th May 2026

India’s English-language newspaper market is showing signs of divergence, rather than moving in a uniform direction of growth or decline.

The latest circulation data suggests a sector recalibrating itself around a narrower set of growth levers, where performance is increasingly tied to city-level dominance, distribution efficiency and audience segmentation. While some publishers are managing to expand circulation modestly, others are witnessing a gradual softening, even as the broader industry grapples with structural headwinds.

This uneven trajectory is reflected in the data from the Audit Bureau of Circulations (ABC) for July–December 2025, available exclusively with e4m.

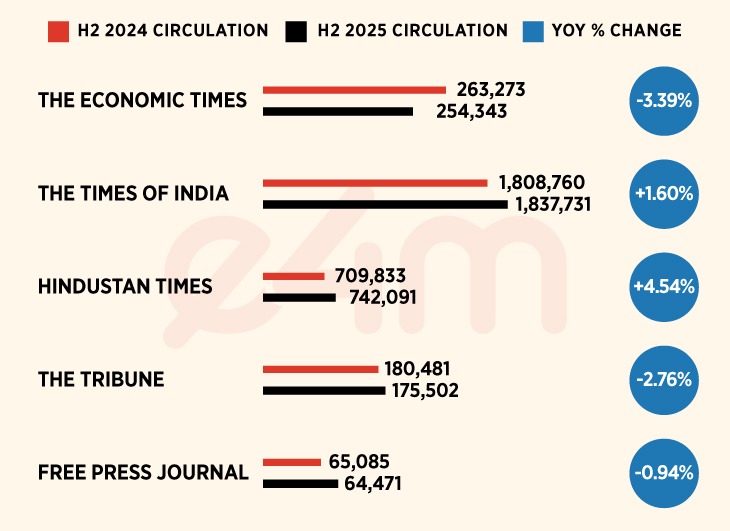

According to the data retrieved by e4m, while Hindustan Times (HT) and The Times of India (TOI) reported year-on-year growth, The Economic Times (ET) and The Tribune saw declines. The Free Press Journal (FPJ), meanwhile, continues to operate with a sharply concentrated regional footprint, with largely stable circulation.

HT reported a total circulation of 742,091 copies in H2 2025, up 4.54% from 709,833 copies in the year-ago period. TOI grew 1.60% to 1,837,731 copies, adding 28,971 copies. In contrast, ET declined 3.39% to 254,343 copies, while The Tribune fell 2.76% to 175,502 copies from 180,481 copies a year earlier.

The Free Press Journal and its associated Free Press editions reported a combined circulation of 64,471 copies in H2 2025, compared to a combined 65,085 copies in the year-ago period. This reflects a marginal decline of 0.94%, indicating largely stable performance despite its concentrated market presence.

These shifts come against a broader backdrop of pressure on print. According to the EY M&E Report 2026, circulation revenues declined by around 1% in 2025, marking the second consecutive year of contraction. For most publications, revenues either remained flat or fell, underscoring the limited headroom for growth in the current environment.

Metro concentration defines the growth story

A closer reading of the ABC data shows that growth, where it exists, is increasingly tied to depth in core urban markets rather than expansion across geographies.

HT’s performance is overwhelmingly anchored in the National Capital Region (NCR). The New Delhi district alone accounted for 579,618 copies, supported by a combination of main and multiple variant editions. Gurgaon added 70,370 copies, while Faridabad, Ghaziabad and Noida contributed smaller but meaningful volumes. The concentration of circulation within NCR highlights the publication’s stronghold in a single high-density market.

TOI follows a similar metro-led model, albeit at a larger scale and with a more diversified urban footprint. Delhi remains its largest centre with 457,458 copies, followed by Bengaluru at 382,868 copies. Kolkata, Hyderabad and Pune further contribute to its metro-heavy base.

FPJ presents the most extreme case of concentration. Mumbai alone accounts for 49,246 of its 64,471 copies, contributing over three-fourths of its total circulation. Its presence outside Mumbai is limited to Indore and nearby markets, indicating a tightly focused regional strategy.

The Tribune, while declining overall, continues to maintain a strong presence in North India, reflecting a regional concentration model that sits between national spread and hyper-local focus.

ET, in contrast, shows a more evenly distributed presence across cities such as Chennai, Hyderabad and Kolkata. However, none of these markets individually contribute outsized volumes, and the relatively tight clustering of figures suggests a balanced but modest scale.

The emerging pattern indicates that scale in English print is increasingly being built through dominance in select metros rather than broad-based national expansion. Publications that are able to consolidate leadership in key urban clusters appear better positioned to sustain or grow circulation.

Variants, distribution and execution as growth levers

Another clear differentiator across publications is the role of variant editions and distribution intensity.

Both HT and TOI rely significantly on variant editions to drive incremental circulation. These variants allow publishers to segment audiences within cities and tailor content and distribution to specific micro-markets. In dense urban regions, this approach can meaningfully expand reach without requiring entry into new geographies.

HT, in its response, told e4m that it would attribute the circulation expansion to “the strength of the brand, based on a century of consistently providing credible and high-quality information, along with a relentless focus on execution across all circulation channels to increase readership.”

The company further said that it continues to work closely with its distribution network, built over several years, to grow copies across its publications.

TOI’s circulation structure also reflects a strong contribution from variant editions across key cities, reinforcing the importance of segmentation in its growth strategy.

In contrast, ET and FPJ do not report significant reliance on variant editions in the available data, indicating a greater dependence on main editions. This points to a more traditional distribution model, which may limit their ability to capture incremental gains in highly competitive urban markets. The Tribune, too, appears to follow a largely main-edition-driven approach, aligned with its regional positioning.

e4m reached out to TOI and FPJ for comment but had not received a response at the time of publishing.

Industry observers suggest that solving for circulation is increasingly operational. Strengthening last-mile delivery, maintaining vendor relationships, and improving distribution efficiency are becoming as critical as editorial positioning.

The EY report echoes this shift, noting that the industry is likely to prioritise retention alongside reach, with distribution challenges expected to be addressed through more focused execution.

An ageing readership and a narrowing growth path

Beneath these circulation trends lies a deeper structural shift in readership behaviour.

According to the EY M&E Report 2026, newspapers are increasingly being consumed by older demographics, typically those aged 35 and above, while younger audiences continue to migrate to digital platforms for news consumption. This generational divide is reshaping how publishers think about growth.

With fewer new readers entering the print ecosystem, the emphasis is shifting towards retaining existing audiences and increasing engagement within core segments. This, in turn, is influencing content strategies, with a greater focus on premium, credible and differentiated journalism.

The report also highlights that circulation revenues have now declined for two consecutive years, suggesting that print growth will remain constrained in the near term. In this environment, expansion into new markets is becoming less viable compared to strengthening presence in existing ones.

For magazines and certain print segments, the report points to premium and exclusive content as a key lever going forward, a principle that is increasingly relevant for newspapers as well.

The fact of the matter

Taken together, the ABC data underscores an English print market that is evolving rather than shrinking uniformly.

HT and TOI demonstrate that growth is still possible, but largely within defined urban strongholds and through variant-led strategies. ET and The Tribune reflect the challenges of sustaining circulation amid broader shifts in consumption, while FPJ illustrates the limits and resilience of a highly localised model.

As digital consumption continues to expand, the future of print circulation is likely to be shaped less by scale alone and more by how effectively publishers can combine distribution strength, audience retention and market focus.

In that sense, the battle for circulation is no longer national, it is increasingly being fought city by city, and in some cases, neighbourhood by neighbourhood.